[Mindset Change #6] - Understand risks - at least don't ignore them

Understanding risk is often ignored and deserves more attention

“Where there is return, there will be risk” - we all know this. Deep down you know that risk and and returns are two sides of the same coin and when evaluating an investment, you should spend 50% time on each aspect. But for most of us, the the effort we spend on understanding risk : return, is more like 5% : 95%, rather than 50% : 50%.

We don’t think too much about risk because it is easier to talk about returns - its quantifiable, sexy and discussed everywhere around us. But ‘risk’ is a boring and fuzzy, something that’s better swept under the carpet. In this chapter I will try to demystify risk and make you more informed about it. “Understand risk and don’t ignore it” is the key mindset change I intend to drive.

In the good times, risk is ignored

At the time of writing (Mar 2022), we are in the midst of more than decade long bull market. Interest rates have been falling for 30 years (see note 1) and most of the investments have given good returns - stocks, bonds, real-estate, VC funds etc - everything.

Especially in the last 2 years, markets have seen a ferocious rally in everything. It’s in times like these when people throw caution to the wind. FOMO rules the narratives and people try to catch the fastest trains without worrying about the risks. Evaluate if you are in a similar mindset, now let’s zoom out and look at the bigger picture.

Why worry about risk?

“Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1” - Warren Buffett

If you are thinking like a VC or starting a business, the above rule doesn’t apply. Otherwise it’s important to be cautious of big losses. Because as a long term investor, your objective is to stay invested, be disciplined and let compounding do its magic. But if you do something crazy and take blind risks, it can lead to a large loss which throw you off the track.

And yes - like me - maybe you also think you are special and crazy risks will not blow up in your face. But the reality is nobody is special, assume risks will come and throw unpleasant surprises at you.

Large Losses are still fine as long as you avoid risk of ruin

Imagine you are in 2008 working as an investment banker in Mumbai. Seeing tremendous potential in the markets, you invest 1 crore of your money in some micro cap companies. Things are going well and you feel so confident that you borrow another 1 crore from a bank and invest the total 2 crores in the stock market.

Then Lehman crisis hits, you lose your job and the stock portfolio fall by 50%. Since you don’t have new money coming from the job, you are forced to sell all your stocks to repay the 1 crore loan - and you are left with zero. The markets will eventually recover, but your wealth will not.

So the first basic principle is to avoid getting yourself into such a situation where you will be ‘forced’ to sell your investments when the chips are down. Way to ensure this is to not invest on borrowed money and not to go all-in on something speculative that can potentially become zero (like some exotic alt-coin you don’t fully understand).

Some Examples of Risks

There are many kinds of risks that can spring a surprise on your investments. Nothing better than live examples to bring them to life. So here are some risks which you are likely to come across in your investments -

Business Risk

This is a simple one. There can be lots of risks because of which a business can go bust. Let’s take the example of Vodafone Idea, from being a formidable player in Indian Telecom space, it has come to the verge of bankruptcy. The problem was that the company couldn’t compete with like of Airtel and Jio and lost market share.

This is also applicable for other investments like Real Estate. The previous start-up where I worked was housed in a nice 15 storey commercial building. But in my observation of 5 years, the building didn’t have more than 30% occupancy - because better projects at better locations became available. People who invested in the properties there had to rent out the space at throw-away prices and overall lost money.

Industry Risk

Sometimes the entire industry in which a company operates can be risky. When I used to work in JP Morgan, I used to do research on US-based coal mining companies. In the 2.5 years I spent there, the market cap of all these coal companies went down by 70% and many became bankrupt. The problem was that coal mining industry was in a decline as US government want to shift its power generation dependency towards cleaner fuels.

There are many industries that are in a decline today or near future - like newspapers, stationery, cable TV, bookstores, FMCG distributors, insurance agents, brick and mortar banks etc.

Valuation Risk (must read) -

This one is grossly misunderstood and widely ignored. In investing, an enduring principle is “everything makes sense at a price”.

So if you are investing in the next hot industry of tomorrow - electric vehicles, plant-based meat, Web3, speciality chemicals - do take a pause and ask yourself - “at what price will this investment not make sense”? Because if you buy something at a price that is much higher than what it is worth, you can lose a ‘lot’ of money.

Let’s take an example of Freshworks, the poster-child of Indian SaaS companies. The company went for an IPO in the US markets in Sep 2021 and it was a successful one. Who would want to miss out on a multi-decade growth story, the Infosys of Indian SaaS. But within six months of the IPO, the stock is down 64%. The business has been doing fine all this while, the problem is that the investors realised the company’s valuation was very expensive and reality caught up.

There are hundreds of examples like this. Sometimes, the entire stock market can become grossly overvalued. Take the case of Japan - the entire market is yet to recover to its peak levels of early 1990s. Someone who bought at the top has not recouped his investment even 30 years after the event.

Valuation risk is important for all kinds of investments, not just stocks. And I would add it is especially a big and ignored risk in the world of Crypto (will share my thoughts in a later chapter). Remember - subjective stories are good, but they need to backed by objective valuation numbers.

Fraud Risk

This is also quite common and under-appreciated fact of investing. When stories become hot, people drop their guard and become blind to risks. When I used to work in Ambit Capital, I was doing research on a hot cloud computing services company based in India. We spoke with the CEO, he sold the story well and everything looked good. But I took a close look at the annual report and found many consistencies, even basic stuff like balance sheet items were not adding up. We flagged the risk and decided to avoid recommending this stock to clients. Two years down the line, auditors unearthed a fraud and entire value of the company was wiped off.

You are probably under-appreciating this fact. Fraud is a genuine risk when you are investing in smaller/less-reputed stocks or real-estate properties in India. The landscape if full of landmines and avoiding them is my value-add as an investor.

Misaligned Incentives Risk -

It may sound similar to fraud risk, but it’s different. Take the case of Hindustan Petroleum (HPCL). It’s one of the stocks I own and recommended in my smallcase portfolio (see note 3).

It’s currently facing some challenges from mis-aligned incentives. Let me explain. The company is majority owned by the Indian government and its core business is to import crude, refine it into fuels and sell it at petrol/gas stations across India. The business is good, valuation is cheap - but the incentives of Indian government is sometimes not aligned with the investors.

At the time of writing (March 2022), the oil prices have surged due to Russia-Ukraine conflict and other factors. Ideally, HPCL should increase the prices of petrol and diesel in line with proportionate rise in global crude prices. However, HPCL is taking losses because the government has advised against raising petrol prices due to ongoing elections in some Indian states.

Such cases of mis-aligned incentives are also commonly seen in other areas. For example, financial advisor may look to maximise their commissions at the expense of investors, real-estate builders may try to minimize costs at the expense of home buyers etc.

Country Risk -

If you are investing in international bonds/stocks - its important to understand country risk.

For example, if you invested in Turkish stocks or bonds - the value of your investment will be down by 75% in last 5 years because of rapid devaluation of the country’s currency - Turkish Lira.

Or let’s take the example of Russia. The country’s stocks have always traded at a discount to other developed markets - and there is a good reason for that. Russia was considered a risky place to do business because of questionable rule of low and threat of sanctions. And since the start of tensions with Ukraine - the Russian stock market has lost 70% of its value.

Regulatory Risk

Changes in regulations can hurt an investment. Sometimes the regulation changes make sense - for example when US regulations favoured cleaner fuels and almost killed its coal mining industry.

Sometimes they regulatory changes don’t make sense. Take the example of Alibaba, which came under severe regulatory crackdown from Chinese government. This was apparently triggered by a speech made by the company’s owner - Jack Ma. Alibaba’s shares are down 65% from peak.

Bitcoin investors should especially be cognizant of regulatory risks.

Liquidity Risk -

I am not being technically correct here, but sometimes you can’t get out of your investments when you need money because of liquidity risk.

For example, many people invested in relative safe - debt mutual funds - of Franklin Templeton in India. But one day, investors got a rude surprise when it was announced the fund is closing and investors cannot make any redemptions. This was because the fund was facing a short term liquidity crunch (see note below).

Or take the case of penny stocks like TTML, that have a track record of occasionally hitting circuit levels and you can’t get out when you want to.

Many of my friends are investing in start-ups these days. Its important to note that start-up investing has a lot of risk around liquidity and one should put only excess disposable money there after all needs are taken care of.

Many other risks -

There are lot many risks with investments.

There is counter party risk where a bank, stock broker, crypto exchange goes bust and you lose your money.

There is key man risk - imagine what will happen to Tesla’s stock if Elon Musk leaves the company because of health or other reasons.

There is an emerging category called - password risk - where you can get locked out of your bitcoin if you forget your private key.

There is also what I like to call investment manager fees risk - where an incompetent investment manager who charges 2% per year can make you lose 20% per over ten years if he fails to perform better than benchmark.

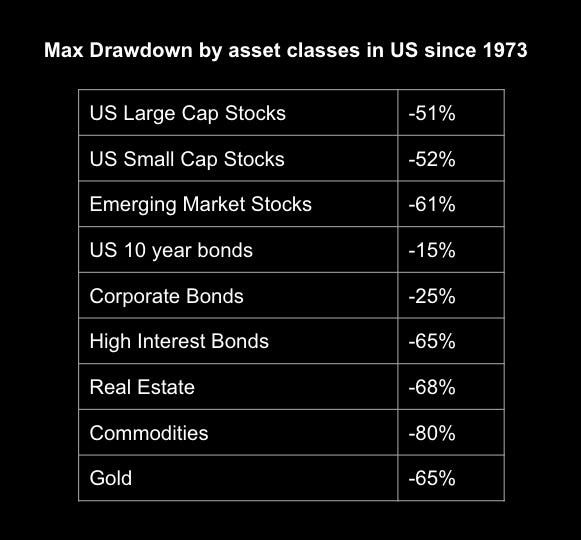

Max Drawdown - a good rule of thumb for measuring risk!

Many people have tried and concluded there is no reliable way to accurately measure risk in terms of numbers. Returns are easy to calculate, risk it not. But one metric which is fairly reliable is - maximum drawdown - how much can an investment fall based on past track record.

The chart below gives a sense of past drawdowns seen in different asset classes over last 50 years in US.

Key takeaways -

Large Cap doesn’t really mean its ‘safer’ than smallcaps.

You can lose money in bonds and gold as well - they are safer but not risk-free.

Real Estate and can be risky as well.

Take risks, but understand them

Don’t become so worried about risks that you become a pessimist. I just want you to not take blind risks and be better informed about them. If you are playing for the long term, you cannot take a large losses by ignoring obvious risks - and you should definitely avoid putting your self into a situation where you risk losing all the money.

Being more informed will help you avoid landmines and also help you to confidently ride through periods when your investments are in losses.

How I manage risk of large losses?

I manage a portfolio on smallcase where I have a plan in place to avoid large losses. They are -

20% allocation to gold as a natural hedge (working well in current Ukraine conflict)

40% allocation is to momentum stocks where I will take small losses and get out in case of a downtrend

40% allocation to undervalued stocks, where I am confident that company is worth more and not bothered by temporary drop in stock prices

While keeping a check on large losses, the portfolio aims to beat broader stock market in the long term.

Some housekeeping…

Is your mailbox trying to keep our content away from you! 💔 What can you do about it? Mark this email as ‘not spam’ or move it from your promotions to the primary folder It’s very easy!

Thanks again, and please tell a few friends if you feel like it.

Optional Notes -

1) Interest rates have been falling for 30 years now!

2) In 2020, a large debt mutual fund scheme folded because of liquidity risk